Borrowers are entitled to certain rights and regulations that seek to help them with repayment in case they default on their repayments for a genuine reason. Guidelines put forth by the RBI not only helps banks and financial institutions receive their payments but also protects the rights of borrowers.

What is the impact of loan default ? And legal action can be taken against loan defaulters? Let’s find out.

Also Read: What Happens When Personal Loans are Not Paid in India?

A borrower may be unable to repay his/her loan due to multiple reasons and results in the following -

One of the major repercussions of loan default is that the credit score of the borrower will decrease significantly.

Defaulting or delaying the EMI payment results in lowering of the credit score and will negatively impact the borrower’s future borrowing capacity, preventing him/her from easily getting loans in the future.

Every borrower is entitled to receiving a set number of reminders and notices from the lending institution. If an EMI is delayed once or twice, notices are sent regarding the late payments.

However, if the reminders and notices are not heeded by the borrower and the EMI is not paid despite this, further action may be taken by the lender such as marking the borrower as a Non-performing asset or NPA. This will prevent the borrower from availing any type of loan or credit in the future.

In case notices and reminders do not result in the loan being cleared, lenders may impose penalties on the borrower or even take legal action.

A missed payment of a few days can still be rectified but if the payment has not been made for more than a month or two, it can result in serious damages.

If a collateral has been provided, this may be used as a way to recover the loan by taking possession of the same.

As per the RBI mandate, at no point of time will the borrower’s rights be compromised.

Breach of contract when it comes to loan repayment itself is not a crime but lenders can approach a civil court in order to recover the same.

If a loan has not been repaid for more than 180 days, the lender is allowed to file a case against the borrower under Section 138 of the Negotiable Instruments Act of 1881.

Sometimes unavoidable circumstances prevent borrowers from being able to repay their loan.. Such cases will not be considered as ‘cheating’ but instead the lender may work with the borrower by modifying the repayment circumstances so as to ensure that the loan is repaid.

However, if the intention of the borrower is proven to be fraudulent right at the time of entering into the loan agreement, a criminal case can be filed against the defaulter.

According to RBI, a ‘wilful defaulter’ is one who indulges in-

Any of the above will result in legal action against the defaulter.

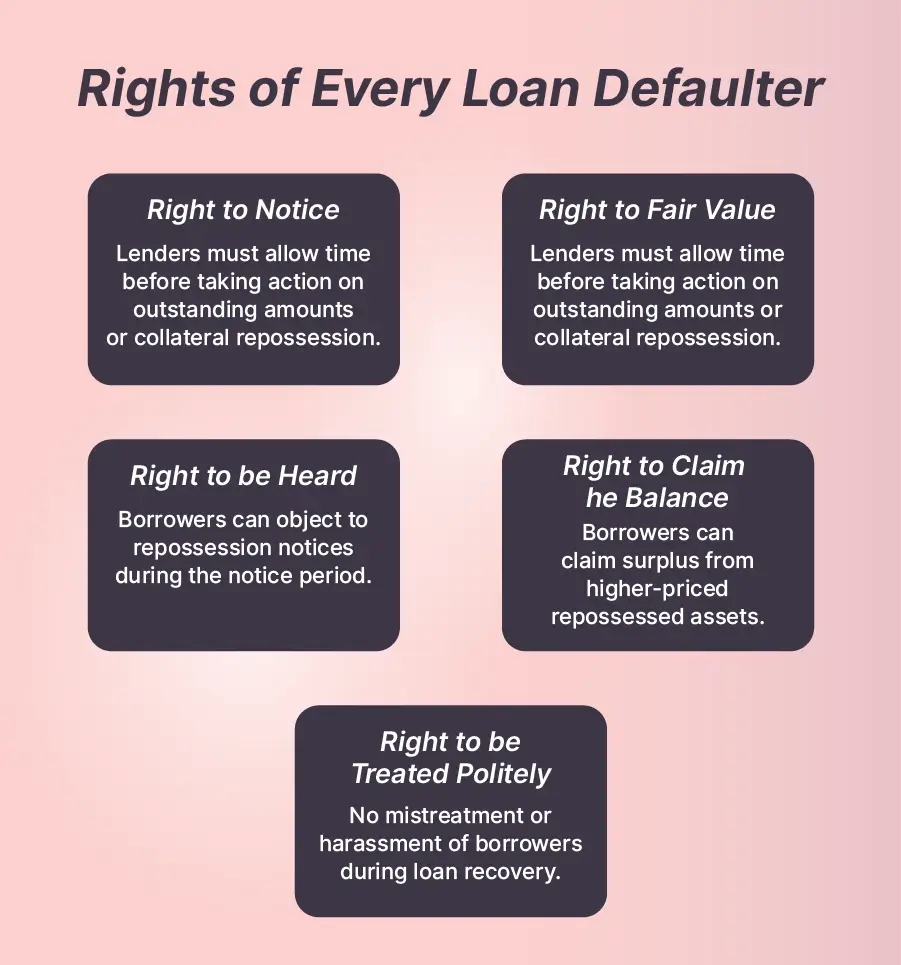

Even if the borrower is unable to repay the loan then he/she does have certain rights in place. These are:

The borrower must be given enough time by the lender before taking action to recover the outstanding amount or repossessing the asset provided as collateral

If the borrower is unable to repay the loan and the lender has repossessed the assets provided, the value cannot be solely decided by the lending institution. A fair value notice must also be sent to the borrower informing him/her of the sale price that has been evaluated

The borrower has the right to raise objections to the notice of repossession sent by the lender during the notice period.

In case the lending institution is receiving a high price for the asset that has been repossessed by them, the leftover balance can be claimed by the borrower

The borrower cannot be mistreated, harassed, humiliated, or abused during the loan recovery process

Personal Loan by Income and Purpose

Personal Loan Insights and Guides

Loan EMI Calculators

Loan Schemes and MSME Loans

Best Personal Loan Resources

Personal Loan in Top Cities

Personal Loan Types and Comparisons

Loan Process, Terms and Rules Explained

Disclaimer

The starting interest rate depends on factors such as credit history, financial obligations, specific lender's criteria and Terms and conditions. Moneyview is a digital lending platform; all loans are evaluated and disbursed by our lending partners, who are registered as Non-Banking Financial Companies or Banks with the Reserve Bank of India.

This article is for informational purposes only and does not constitute financial or legal advice. Always consult with your financial advisor for specific guidance.

Was this information useful?