How to Get a Home Loan through Moneyview

1

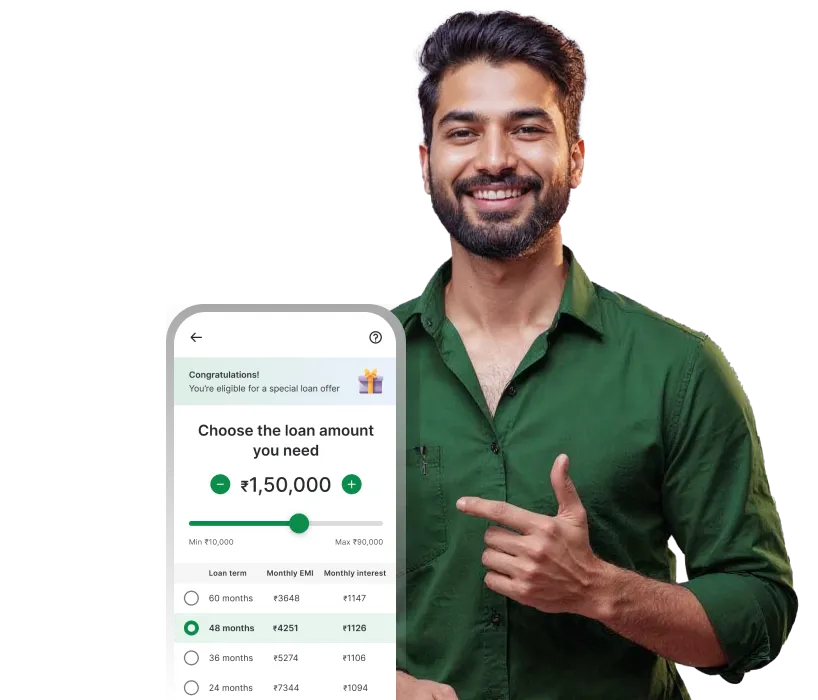

Enter personal details and submit application

2

Lending partner calls you to confirm details

3

Site visit and in-person discussion

4

Loan approval and get funds disbursed

Formula to Calculate Home Loan EMI

In case you are interested to know the formula that all house loan calculators use, here it is -

E = P x R x (1+R)^N

————————

[(1+R)^N-1]

P - the principal amount that is borrowed

R - the rate of interest imposed

N - tenure in the number of months

Here is an example -

Let Rs.10,00,000 be the amount borrowed (P), the annual rate of interest (R) be 8% , and 3 years or 36 months be the tenure (N)

Then the EMI to be paid using the above formula will be:

E = [10,00,000 x 0.00666 x (1+0.00666)^36] / [(1+0.00666)^36-1] = Rs. 31,336

Therefore, the EMI for a Rs.10 Lakh home loan would be Rs.31,336.

The rate of interest (R) is calculated monthly i.e. it is calculated as (Annual Rate of interest/12/100). In this case, it is 8/12/100 = 0.00666.

The above formula can be used to calculate EMIs for all types of loans and not just home loans, unless mentioned otherwise.

Factors that Affect Home Loan EMI

Credit Score

Thus, if you are planning to take a housing loan in the future, it is advisable to start working on improving your credit score.

Location and Value of the House

MCLR Rates

This is decided annually and depends on various factors such as operating cost, the marginal cost of funds, etc. The interest rate imposed will increase or decrease based on variations in the MCLR rate.

Loan to Value or LTV Ratio

Employment Status of Applicant

Repayment Tenure

Personal loan related links

Loan on Aadhaar & PAN Card

Personal Loan Interest Rates

Personal Loan Eligibility

Personal Loan Documents

Personal Loan For Self-Employed

Personal Loan for Salaried Employees

Home Loan EMI Related FAQs

What is a home loan?

How do banks calculate interest on home loans?

There are many factors which affect the calculation of interest rate on home loans. Some of the factors are mentioned here-

- Applicant's credit score

- Valuation of the house

- Age and income of the applicant

- Repayment tenure

- Principal amount borrowed

- Debt-to-income ratio

What is the EMI for a Rs. 40 Lakh home loan?

EMI = [P x R x (1+R)^N ] / [(1+R)^N-1]

Let's say that the tenure of your 40 Lakh loan is 6 years and the rate of interest is 8%. Then, your monthly EMI will be -

E = [40,00,000 x 0.00666 x (1+0.00666)^72] / [(1+0.00666)^72-1] = Rs. 70,133/-

What is the difference between flat balance and reducing balance interest calculation?

EMI calculation can be made in two ways i.e., the flat balance or reducing balance interest method.

- If the interest amount payable is based on the entire loan amount for the full duration of loan repayment, it is known as flat balance interest calculation. In this case, the EMI amount remains the same during the tenure.

- In case of the reducing balance interest rate calculation method, the interest is calculated on the outstanding principal amount each time after the payment of an installment. In this method, the EMI keeps changing throughout the tenure.

What is the EMI for a 20 Lakh home loan?

EMI = [P x R x (1+R)^N ] / [(1+R)^N-1] {where, P is the principal amount, R is the rate of interest, and N is the number of months in your tenure}

Thus, EMI = [20,00,000 x 0.00666 x (1+0.00666)^36] / [(1+0.00666)^36-1] = Rs.62,673/-

How much home loan can I get on Rs.25,000 salary?

The amount you can avail as home loan depends on multiple factors as mentioned previously. These include -

- Your credit score

- Monthly income

- Debt-to-income ratio i.e., the amount of debt you are paying off with your existing salary

- The cost of your home also matters. Generally, lenders offer up to 90% of the price of the property as loan

- The amount you pay as down payment. Higher the down payment amount, lower will be the loan to be availed

- The repayment term and interest rate imposed. Remember, higher the repayment tenure, higher is the overall interest amount paid.

Can you get a home loan if you are retired?

Can you have more than one home loan at a time?

You can definitely have more than one home loan at the time. There is no law in India that states that you can only have one home loan at a time. Taking multiple home loans will depend on a lot of factors, the most important being -

- Your credit score

- Your debt-to-income ratio

- Your income and age

Click here

Get an instant personal loan from Moneyview

Download the app now from Google Play

Disclaimer

The starting interest rate depends on factors such as credit history, financial obligations, specific lender's criteria and Terms and conditions. Moneyview is a digital lending platform; all loans are evaluated and disbursed by our lending partners, who are registered as Non-Banking Financial Companies or Banks with the Reserve Bank of India.

This article is for informational purposes only and does not constitute financial or legal advice. Always consult with your financial advisor for specific guidance.